Under U.S. GAAP, interest paid and received are always treated as operating cash flows. The Company uses Adjusted EBITDA and Adjusted EBITDA margin, among other measures, to evaluate the Company’s operating performance. Adjusted EBITDA is among the primary measures used by management for the planning and forecasting of future periods, as well as for measuring performance for compensation of executives and other members of management. We believe this measure is an important indicator of the Company’s operational strength and performance of its business because it provides a link between operational performance and operating income. It is also a primary measure used by management in evaluating companies as potential acquisition targets. Digital Audio revenue increased $33.8 million, or 12.7%, driven primarily by continuing increases in demand for digital advertising.

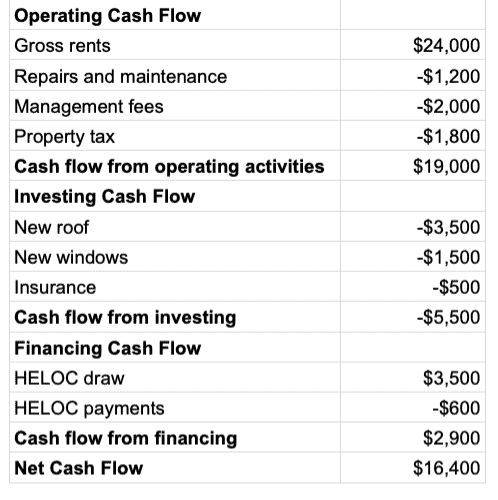

Investing Cash Flow

A cash flow statement (CFS) is a financial statement that captures how much cash is generated and utilized by a company or business in a specific time period. Cash flow statements are one of the most critical financial documents that an organization prepares, offering valuable insight into the health of the business. By learning how to read a cash flow 5 tax tips for the newest powerball millionaires statement and other financial documents, you can acquire the financial accounting skills needed to make smarter business and investment decisions, regardless of your position. Based on the cash flow statement, you can see how much cash different types of activities generate, then make business decisions based on your analysis of financial statements.

Accounting Research Online

You use information from your income statement and your balance sheet to create your cash flow statement. The income statement lets you know how money entered and left your business, while the balance sheet shows how those transactions affect different accounts—like accounts receivable, inventory, and accounts payable. Information about all material investing and financing activities of an enterprise that do not result in cash receipts or disbursements during the period appear in a separate schedule, rather than in the statement of cash flows. For instance, assume a company issued a mortgage note to acquire land and buildings.

What is the difference between direct and indirect cash flow statements?

The third section of the cash flow statement lists the information for the company’s financing activities. Financing activities include purchases of bonds and stock as well as dividend payments. Some of the applicable ledger accounts include your capital equipment and paid-in capital accounts, notes and bonds payable, stock and retained earnings. Operating activities are those involved in the day-to-day running of the business. Accounts used for operating activities include all those on the income statement as well as current assets and current liabilities on the balance sheet. (Current assets and liabilities are those that are expected to be converted to cash within one year.) Most of a business’ transactions are operating activities.

- Financial documents are designed to provide insight into the financial health and status of an organization.

- After calculating cash flows from operating activities, you need to calculate cash flows from investing activities.

- In our examples below, we’ll use the indirect method of calculating cash flow.

- Having negative cash flow means your cash outflow is higher than your cash inflow during a period, but it doesn’t necessarily mean profit is lost.

- Since we received proceeds from the loan, we record it as a $7,500 increase to cash on hand.

Others treat interest received as investing cash flow and interest paid as a financing cash flow. Cash flows resulting from the financing activities of the company are shown under the financing activities section of the statement of cash flows. Financing activities mostly include those activities that change the size and composition of the equity (i.e., common or preferred stock) and the long-term liabilities (i.e., long-term loans and borrowings) of the company. Besides this, short-term loans obtained from commercial banks or other financial institutions with the purpose of acquiring capital or funding the company’s business are also considered a financing activity. During the reporting period, operating activities generated a total of $53.7 billion.

Cash Flow Statement Direct Method

Cash flow statements are one of the three fundamental financial statements financial leaders use. Along with income statements and balance sheets, cash flow statements provide crucial financial data that informs organizational decision-making. While all three are important to assessing a company’s finances, some business leaders might argue that cash flow statements are the most important. With the indirect method, cash flow is calculated by adjusting net income by adding or subtracting differences resulting from non-cash transactions.

However, this could also mean that a company is investing or expanding which requires it to spend some of its funds. Other companies may also have a higher capital investment which means they have more cash outflow rather than cash inflow. The cash flow statement presents a good overview of the company’s spending because it captures all the cash that comes in and goes out. This is another example of a cash flow statement of Nike, Inc. using the indirect method for the fiscal year ending May 31, 2021. This method of calculating cash flow takes more time since you need to track payments and receipts for every cash transaction.

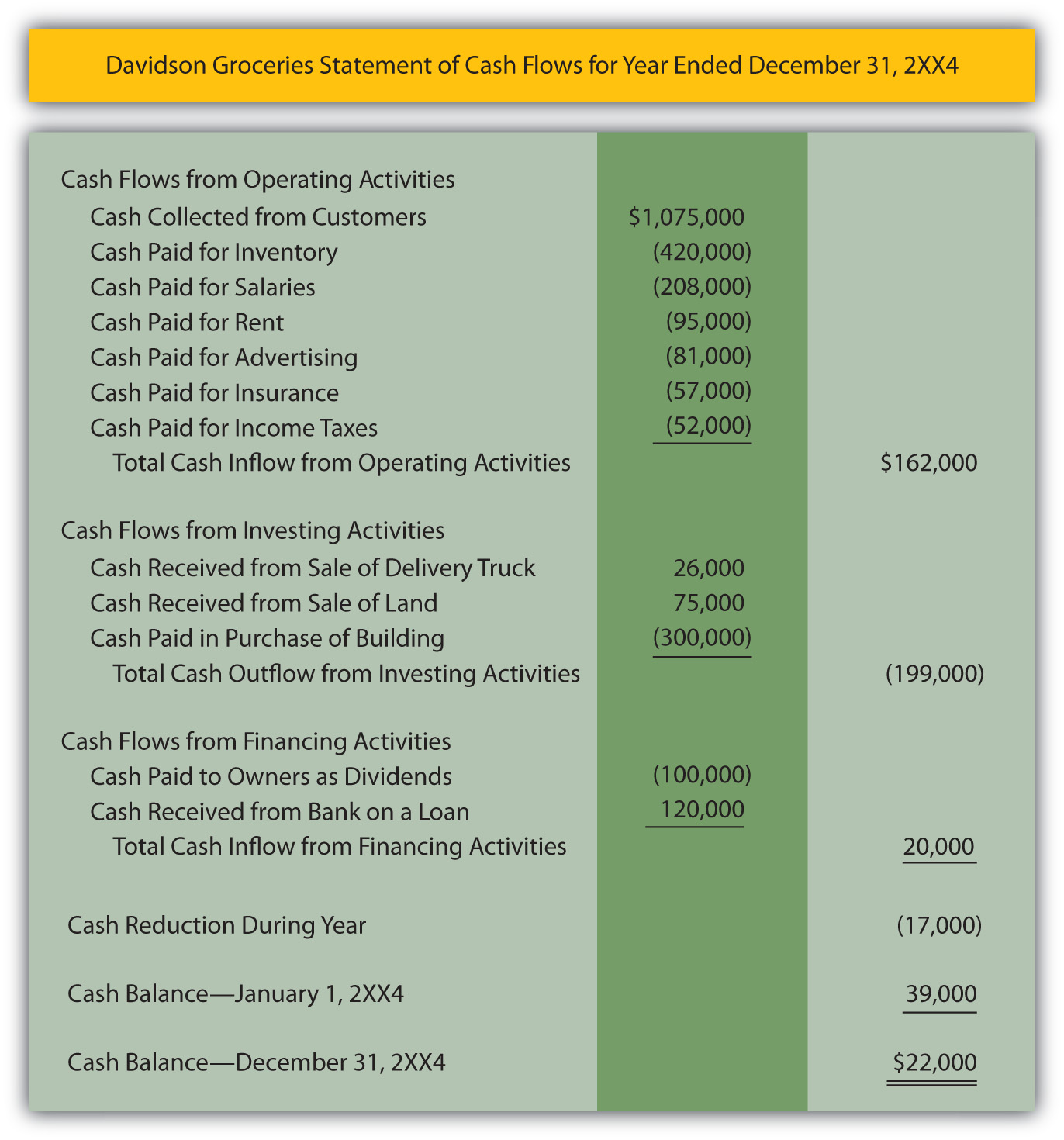

The operating activities section of the statement of cash flows appears first. It may be prepared in one of two ways, using either the indirect or the direct method. Although information presented in the operating activities section is different, both methods yield the same cash flows from operating activities amount. The indirect method is more popular because the information needed to prepare the section is readily available on the income statement and balance sheet. The investing and financing section both are prepared using a direct method.

The final task to wrap up the statement of cash flows is to tally net cash generated or used by summing all three sections. This amount is then used to adjust the beginning cash balance from the balance sheet. Assuming the statement was prepared correctly, the sum should equal the ending cash balance on the balance sheet. It is useful to see the impact and relationship that accounts on the balance sheet have to the net income on the income statement, and it can provide a better understanding of the financial statements as a whole.